11 Best Leading Indicators for Day Trading You Should Know

Discover the best leading indicators for day trading to spot trends early and make smarter trading decisions with greater confidence.

Ever watched a trade slip away because your indicators lagged and your entry felt like a guess? Trading Patterns show how price, volume, and momentum line up before a move, giving early clues you can act on. This guide highlights the best leading indicators for day trading, from RSI, MACD, and stochastic oscillator to VWAP, moving averages, volume profile, order flow, ATR, and volatility tools, and explains how to use divergence, breakout signals, support and resistance, and price action to time entries and confirm signals. You will get clear setups, backtesting tips, risk management rules, and practical steps to boost win rates and scale profits with real funded capital.

To put those skills to work, Aquafutures offers funded accounts for futures trading so you can trade real capital while sharpening entries, sizing positions, and growing returns.

Summary

- Turn indicators into rule-based setups rather than mystical signals. The article highlights 11 practical leading indicators and reports that 50% of day traders rely on RSI for entries.

- Combine indicators into explicit binary gates to reduce false breaks, supported by findings that over 50% of successful day traders use combinations of leading indicators and that 70% of traders use moving averages as a common tie-breaker.

- Validate every signal like an experiment, running realistic replay with order types, slippage, and a minimum sample size of at least 200 trades before trusting live results.

- Enforce operational discipline and patience, for example, master one core setup for 30 trading days, require at least 100 checklist-compliant simulated trades before scaling, and log every deviation for audit.

- Test scalability with stepped notional runs, since controlled replays showed doubling size without widening stops halving fill quality, and capacity checks must track slippage, fill rates, and expectancy as size rises.

- Measurement and maintenance are critical, given that 50% of organizations report difficulty measuring leading indicators. Run monthly audits, monitor decay over 30-, 60-, and 90-day windows, and require human sign-off for any parameter change.

- Aquafutures's funded accounts for futures trading address this by letting traders apply validated indicator rule sets to live capital under structured evaluation and realistic execution testing.

11 Best Leading Indicators for Day Trading

These 11 indicators are practical tools you can combine into repeatable, low‑ambiguity setups that flag entries, confirm momentum, and define stops, enabling performance to be measured and scaled. Use them as rule‑based building blocks, not as mystical signals, and you turn noisy intraday moves into verifiable edges you can validate in simulated capital.

1. Relative Strength Index (RSI)

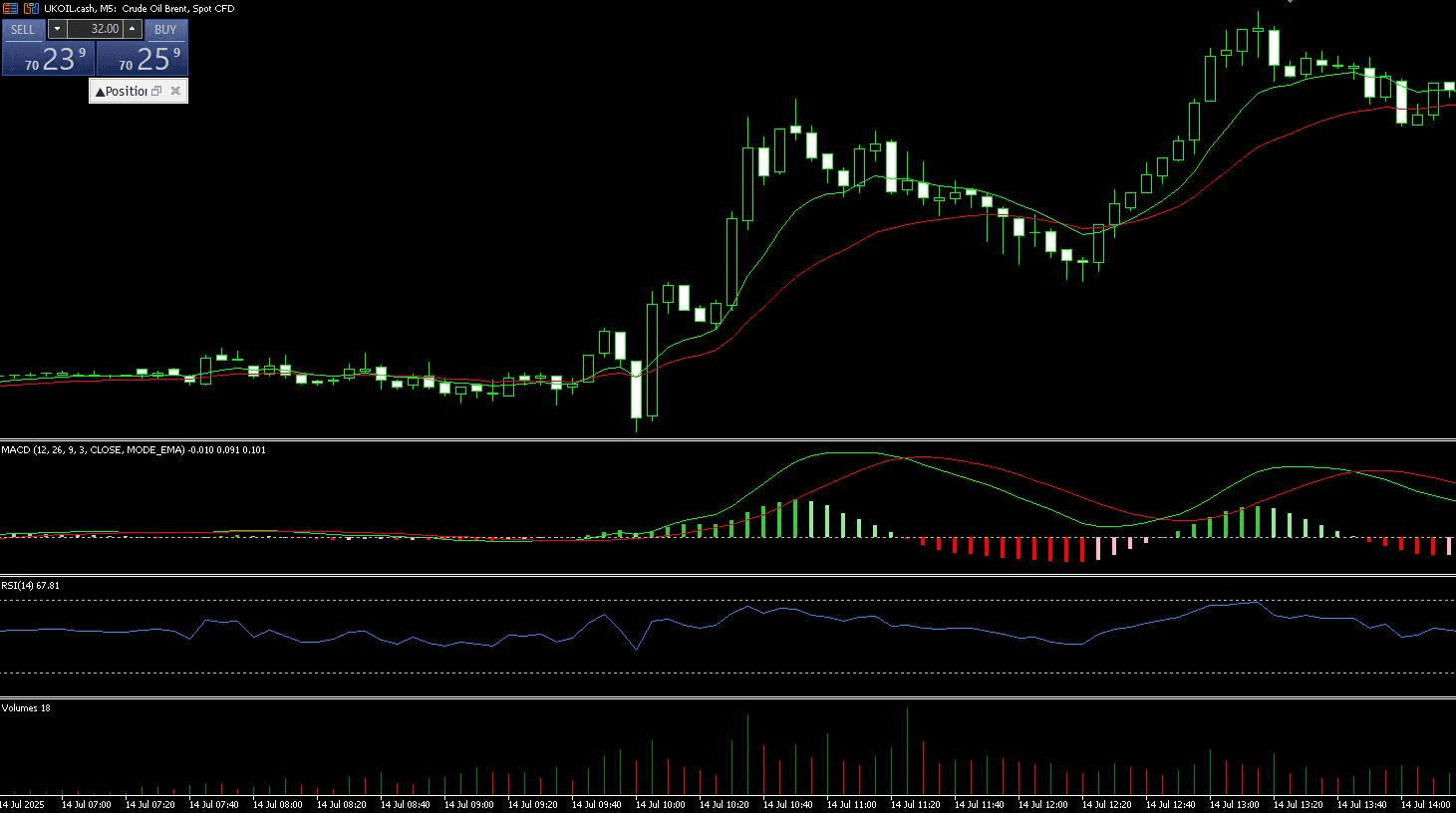

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and magnitude of recent price changes. It ranges from 0 to 100 and is designed to indicate when a market is overbought (extended to the upside) or oversold (extended to the downside). Classic reference levels are 30 and 70, but intraday traders often tweak those levels to fit volatility and the asset’s personality. RSI is popular among day traders because it reacts quickly to short bursts of buying or selling pressure. That rapid feedback can flag potential turning points before the price fully reverses. On lower-timeframe charts such as 1‑minute, 5‑minute, or 15‑minute, RSI can generate frequent signals, which is crucial for traders who need multiple opportunities throughout the session.

How Day Traders Use This Indicator

Day traders typically look for long setups when RSI dips below 30 and then turns back up, signaling that downside momentum may be fading. In strong intraday uptrends, some traders raise the oversold threshold to around 40 to avoid fighting the trend. For short trades, they watch for RSI to push above 70–80 and then roll over, suggesting that buyers may be exhausted. RSI is also used for divergence. If price prints a new high but RSI forms a lower high, traders interpret it as a warning that momentum is not confirming the move and that a pullback or reversal may be near. The same logic applies in downtrends when price makes a new low but RSI fails to do the same.

What Makes This Indicator Effective

RSI is effective because it compresses momentum into a single, easy-to-read line that reacts faster than many trend indicators. It doesn’t just show direction; it highlights the intensity of recent moves, which is precisely what short-term traders care about when timing entries and exits. It also works well in combination with other tools. When an RSI signal aligns with a clear support or resistance level, a volume spike, or a price pattern, it can significantly improve the probability of a trade. Used this way, RSI becomes less about calling tops and bottoms blindly and more about confirming high-quality setups.

2. Stochastic Oscillator

The Stochastic Oscillator is another momentum-based tool that compares an asset’s closing price to its price range over a chosen lookback period. It typically consists of two lines, %K and %D, which oscillate between 0 and 100, with key zones at approximately 20 (oversold) and 80 (overbought). This structure helps traders visualize whether the price is closing near the high or low of its recent range. Unlike some slower indicators, the Stochastic Oscillator responds quickly to changes in short-term sentiment. That sensitivity makes it especially attractive for day traders working on lower time frames who need timely signals as the market swings between intraday extremes.

How Day Traders Use This Indicator

Day traders generally look for long opportunities when the stochastic reading dips below 20 and then crosses back above that level, especially if the price is sitting near a known support area. For shorts, they look for readings above 80 that curl back down, ideally near resistance. Many intraday traders pay particular attention to crossovers between the %K and %D lines, treating them as trigger signals. Like RSI, traders also watch for stochastic divergence: if the price pushes to a new high but the oscillator fails to confirm it, that can hint at fading buying pressure. Some day traders smooth the settings to filter out noise on speedy time frames, while others keep them fast to catch quick scalping opportunities.

What Makes This Indicator Effective

The Stochastic Oscillator is effective because it focuses on where the price closes within its range, which often shifts before the broader trend is clearly changing. That helps spot potential turning points ahead of time, particularly in choppy or range-bound intraday markets. Its dual-line structure also gives more nuance than single-line oscillators. Crossovers and line slopes add context to simple overbought/oversold readings. When combined with structure (support, resistance, trendlines) and volume, stochastic signals can give well-timed entries with clearly defined risk.

3. Support and Resistance Levels

Support and resistance are price levels where buying or selling interest has repeatedly appeared in the past. Support refers to areas where demand has typically been strong enough to stop declines, while resistance marks zones where supply has historically halted rallies. These levels are not indicators in the traditional “math formula” sense, but they are among the most important leading tools in day trading. Because markets often react to the same price areas multiple times, support and resistance can act as a roadmap for intraday price behavior. Day traders closely track prior day highs and lows, opening ranges, key intraday swing points, and higher time frame zones (from daily or 4‑hour charts) that may influence intraday moves.

How Day Traders Use This Indicator

Intraday traders watch how the price behaves as it approaches these levels. A common approach is to look for long trades when the price tests a well-defined support zone and shows signs of holding (such as rejection wicks, volume confirmation, or bullish candles). Conversely, they look for short setups when the price tests resistance and fails to break through convincingly. Many day traders also plan breakout trades around major levels. If price consolidates just below resistance and then breaks above with strong volume, traders may buy the breakout and use the old resistance as a new support for their stop-loss. The same logic applies to breakdowns below support.

What Makes This Indicator Effective

Support and resistance are effective because they reflect real areas of prior supply and demand where large participants may be active again. Institutions, algorithms, and retail traders all tend to focus on similar reference points (previous highs/lows, round numbers, session opens), which increases the likelihood of a reaction. These levels also provide clear risk management anchors. Traders can define stops just beyond a level and set realistic profit targets at the next logical zone. This clarity often leads to cleaner reward-to-risk profiles, which is crucial for long-term consistency in day trading.

4. Pivot Points

Pivot Points are a set of price levels calculated from the previous period’s high, low, and close. The main pivot (PP) serves as the central reference, and additional support (S1, S2, S3) and resistance (R1, R2, R3) lines are derived from it. Day traders commonly use daily pivot points, recalculated at the end of each session, to map out intraday “zones of interest.” Because professional and retail traders widely use pivot points, they often behave as self-fulfilling levels around which order flow clusters. In fast-moving markets, these levels can highlight where pullbacks might stall, where consolidations may form, and where breakouts could trigger.

How Day Traders Use This Indicator

Day traders overlay pivot points on their intraday charts and pay attention to how the price reacts around the central pivot and the first support and resistance levels. In trending sessions, many traders enter pullbacks that bounce off the pivot or S1/R1 and then ride the move toward the next pivot band. In ranging sessions, pivot levels serve as potential boundaries for mean-reversion trades. Some day traders combine pivot points with candlestick patterns and volume. For example, a strong bullish engulfing candle forming at S1 with rising volume might be treated as a long signal, with PP or R1 as a target. Others use pivot bands to set realistic intraday take-profit levels instead of targeting arbitrary points.

What Makes This Indicator Effective

Pivot points are effective because they compress the previous session’s key price information into a grid of levels that many market participants monitor. This collective attention increases the odds that the price will at least pause or react when it touches one of these lines. They also help traders quickly structure the day: readings above the central pivot are often interpreted as bullish, while readings below it suggest a bearish tilt. That simple framework helps intraday traders stay aligned with the session’s overall tone while looking for precise entries at the surrounding support and resistance bands.

5. Donchian Channels

Donchian Channels are a volatility-based indicator that plots the highest high and lowest low over a chosen lookback period, usually shown as upper and lower bands. A middle line is often added as the average of those two extremes. The result is a visual “price envelope” that tracks the most recent range and expands or contracts as volatility changes. Initially developed for trend-following strategies, Donchian Channels are also useful for active intraday traders. They highlight where price is breaking out of its recent range, where it’s stuck in consolidation, and how strong current directional moves are relative to recent history.

How Day Traders Use This Indicator

Day traders watch for the price to close above the upper band as a signal of a bullish breakout and below the lower band as a sign of a bearish breakout. On shorter time frames, these breaks can mark the start of intraday momentum runs, especially when they align with higher time frame direction or news catalysts. Some traders scale into trades as the price rides the band in the direction of the trend. The middle band often serves as a dynamic reference for pullbacks. In a strong uptrend, traders look for the price to retrace toward the median line and then resume upward, using that area as a potential entry zone. In ranges, traders may fade moves back toward the opposite band, provided there is confirming evidence that the breakout is failing.

What Makes This Indicator Effective

Donchian Channels are effective because they provide a clear, rule-based way to define breakouts and trend continuation. Instead of guessing whether a move is significant, traders can rely on a simple condition: price must exceed the recent highest high or lowest low. This reduces subjectivity and helps create systematic entry and exit rules. They also adapt automatically to changing volatility. When the channel widens, traders know the market is more active and can adjust position sizing and expectations accordingly. When it narrows, they can anticipate potential expansion phases or stay cautious about false signals in tight ranges.

6. Fibonacci Retracement

Fibonacci Retracement draws horizontal lines at key ratios derived from the famous Fibonacci sequence, such as 23.6%, 38.2%, 50%, and 61.8%. These levels map potential reversal zones within a price swing, helping traders pinpoint where pullbacks might end before the original trend resumes. Day traders apply them to intraday swings, often from the session's open or recent highs and lows. The tool's potential lies in its ability to highlight "natural" pause points where price often stalls due to psychological clustering of orders. On fast charts, Fibonacci levels act like magnets, drawing price back to test them before continuing or reversing, which suits the quick decision-making of intraday trading.

How Day Traders Use This Indicator

Day traders plot Fibonacci Retracement from swing lows to highs in uptrends (or highs to lows in downtrends) and watch for the price to retrace to the 38.2% or 61.8% levels. A bounce there with bullish confirmation—like a hammer candle or volume surge—signals a long entry, targeting the 0% or prior high. Stops go below the next Fibonacci level or swing low. For shorts, they target retracements to these levels in downtrends. Many combine it with other signals, entering only when the price respects the level multiple times or aligns with volume. Breakouts beyond the 61.8% often prompt traders to exit or reverse positions.

What Makes This Indicator Effective

Fibonacci Retracement works because these ratios appear repeatedly in market geometry, reflecting how traders naturally divide risk and reward. Large players often defend these levels, creating self-reinforcing reactions that give smaller traders an edge. Its flexibility shines on intraday charts: levels adjust to the session's swings, providing fresh setups without lagging behind price. When stacked with support/resistance or momentum oscillators, it boosts accuracy by confirming confluence zones.

7. Ichimoku Cloud

The Ichimoku Cloud combines multiple lines into one comprehensive view: Tenkan-sen (short-term average), Kijun-sen (medium-term average), Senkou Span A and B (forming the "cloud"), and Chikou Span (lagging line). Price above the cloud signals uptrends, below indicates downtrends, and within suggests indecision. Day traders simplify it for intraday by focusing on cloud interactions and line crossovers. This all-in-one system offers trend direction, momentum, and dynamic support/resistance at a glance, reducing chart clutter. On 5- or 15-minute charts, it filters noise while highlighting shifts in intraday sentiment early.

How Day Traders Use This Indicator

Traders enter longs when the price breaks above the cloud with Tenkan crossing above Kijun, using the cloud's top as support. Shorts trigger on breakdowns below the cloud with bearish crossovers, targeting the cloud's bottom or next thickness. Cloud twists (thinning then thickening) warn of volatility spikes. Day traders also watch the Chikou Span crossing price for confirmation. In trends, they ride price hugging the cloud edge; in ranges, they fade extremes back into the cloud body.

What Makes This Indicator Effective

Ichimoku excels by projecting future support/resistance via the forward-shifted cloud, giving a leading edge over static levels. Its layered components create strong filters—only aligned signals trigger trades—cutting false moves in choppy sessions. The visual cloud instantly conveys bias: thick clouds mean strong barriers, thin ones invite breaks. This holistic view helps day traders align with momentum while managing risk through built-in stop zones.

8. On-Balance Volume (OBV)

On-Balance Volume (OBV) tracks cumulative volume by adding it to a running total on up days and subtracting it on down days. Rising OBV confirms buying accumulation behind price gains; falling OBV reveals distribution on declines. Day traders use intraday OBV to gauge if volume supports price action in real time. Unlike price-alone tools, OBV reveals "smart money" flow early, often diverging from price to foreshadow turns. On tick or volume charts, it shines for spotting hidden strength or weakness during quiet price periods.

How Day Traders Use This Indicator

Day traders seek OBV uptrends during price consolidations for long entries, expecting breakouts. Divergences are key: rising OBV with flat price signals impending upside; falling OBV under rising price warns of shorts. They enter when OBV breaks its own trendline alongside price. Volume spikes aligning with OBV direction confirm setups. Traders exit if OBV flattens, indicating momentum loss, and pair it with price levels for precise timing.

What Makes This Indicator Effective

OBV's effectiveness stems from prioritizing volume as the true driver of sustainable moves—price without volume often fades. It leads by capturing flow before widespread price reaction, ideal for intraday edges. Its simplicity avoids overcomplication, yet divergences provide high-probability reversals. Combined with price oscillators, OBV validates trends, turning volume data into actionable foresight.

9. Accumulation/Distribution Line (A/D Line)

The Accumulation/Distribution Line (A/D Line) measures buying/selling pressure by weighting volume based on where the price closes within its daily range. Close near highs adds to A/D (accumulation); close near lows subtracts (distribution). Rising A/D shows inflow; falling reveals outflow, even if price stalls. For day traders, A/D uncovers subtle shifts in control during intraday ranges, leading price by highlighting pressure builds. It adapts to a close location, making it sensitive to session nuances.

How Day Traders Use This Indicator

Traders watch A/D rising under sideways price for long breakouts, entering on volume confirmation. Bearish divergences—price highs with A/D lows—trigger shorts. They use A/D trend breaks as signals, with stops beyond recent swing points. In trends, A/D pullbacks to its moving average offer re-entries. Pairing with candlesticks refines timing, like bullish closes boosting A/D.

What Makes This Indicator Effective

A/D leads by quantifying "effort" via close-weighted volume, spotting divergences before price cracks. It filters weak moves lacking conviction, crucial for day trading's high noise. The range-based weighting captures intraday psychology accurately, outperforming raw volume. As a confluence tool, it strengthens other signals, enhancing win rates on fast setups.

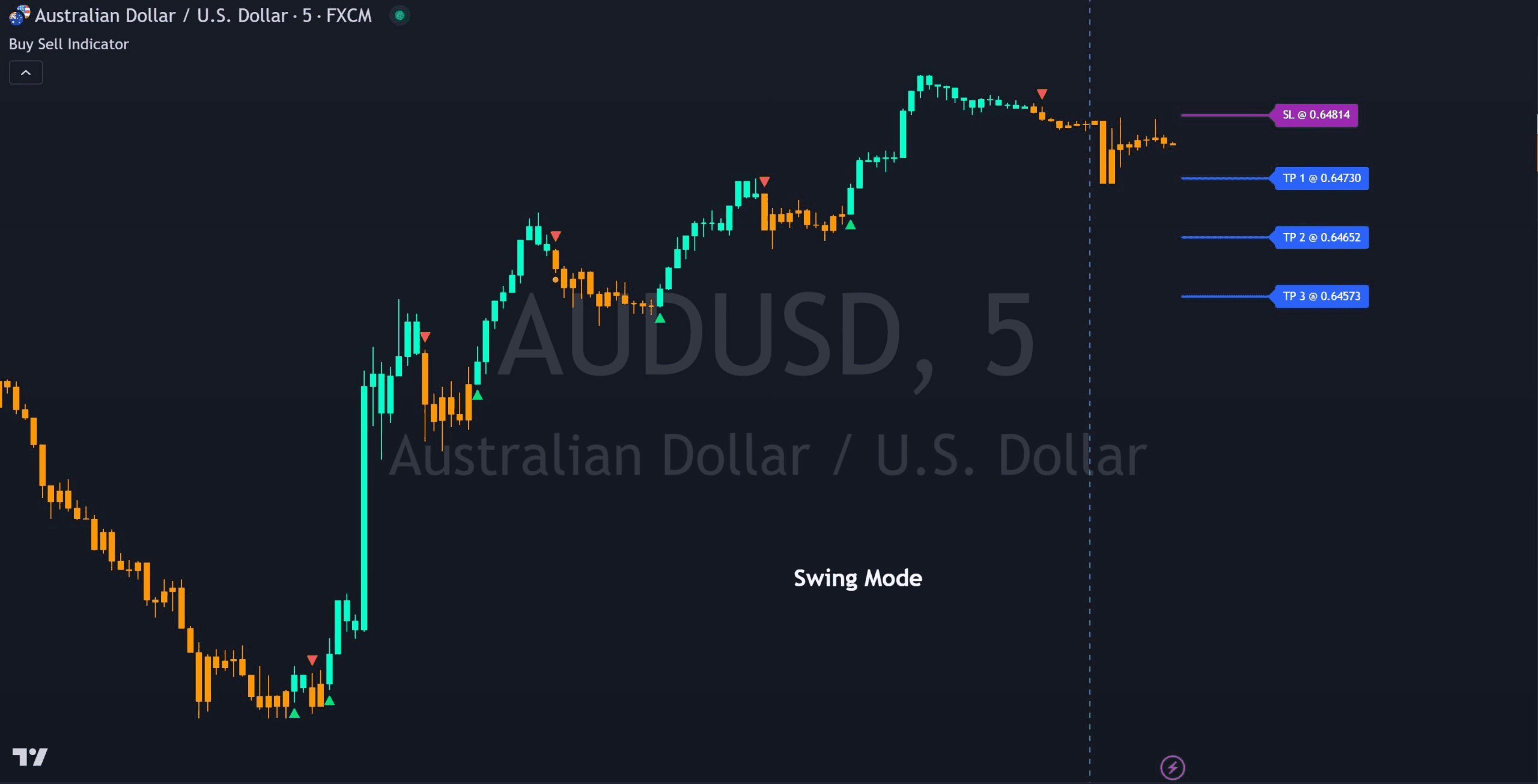

10. Volume Weighted Average Price (VWAP)

Volume Weighted Average Price (VWAP) calculates the average trade price weighted by volume from session start, acting as a dynamic benchmark. Price above VWAP suggests bullish control; below indicates bears. Day traders reset it daily, using it as an intraday "fair value." VWAP's volume emphasis makes it a leading gauge of institutional activity, often bending before price extremes. Anchored resets keep it relevant for scalps and swings.

How Day Traders Use This Indicator

Traders buy pullbacks to VWAP in uptrends, selling rallies to it in downtrends—mean reversion core. Breakouts above/below VWAP with volume signal trend entries, using VWAP as trailing support/resistance. Deviations (e.g., 1-2 standard bands) set targets; extreme stretches prompt fades. Institutions watch it too, amplifying reactions.

What Makes This Indicator Effective

VWAP leads as the session's volume-adjusted median, reflecting true average cost—prices revert to it 70-80% of days. Its universal use creates self-fulfilling behavior. Dynamic updates match intraday flow, providing clear bias (above = bull) and risk levels. Bands add volatility context, perfect for position sizing.

11. Average Directional Index (ADX)

The Average Directional Index (ADX) quantifies trend strength on a scale from 0 to 100, regardless of direction. Readings above 25 signal robust trends, while below 20 point to weak or sideways action. It pairs with +DI and -DI lines to show directional bias, helping traders avoid choppy periods. Day traders value ADX for its ability to filter trades by conviction level. On short time frames, rising ADX warns of emerging momentum, letting traders prioritize trending sessions over range-bound noise.

How Day Traders Use This Indicator

Traders enter longs when +DI crosses above -DI and ADX climbs past 25, confirming upward strength. Shorts trigger on -DI dominance with rising ADX. They exit or avoid trades if ADX drops below 20, signaling fading drive. In combos, ADX validates breakouts: high readings support riding moves, low ones favor scalps at range edges. Stops trail behind DI crossovers for dynamic risk control.

What Makes This Indicator Effective

ADX shines by isolating trend power from direction, preventing whipsaws in low-momentum markets—a day trader's biggest drain. Its smoothing reduces false signals, providing clean "go/no-go" thresholds. Paired with price tools, it boosts edge: strong ADX turns average setups into high-probability plays. Universally respected, it aligns traders with institutional trend participation.

A practical pattern I keep returning to is simplicity with a testable checklist: a trend filter, a momentum trigger, a volume confirmation, and a fixed stop. This fixes two standard failure modes: first, traders chase indicator signals in isolation during high noise; second, they neglect to adjust settings to the instrument and timeframe. This pattern appears across scalpers, prop traders, and swing intraday systems, and the remedy is constraint‑based: when volatility is high, widen thresholds and require volume confirmation; when the market is quiet, tighten filters and prefer mean reversion.

Most traders validate setups using spreadsheets and scattered simulations because they are familiar and low-cost. Still, that approach fragments evidence and stretches verification from days into weeks, creating inconsistent decisions under pressure. Platforms like AquaFutures provide instant simulated capital and structured evaluation rules, letting traders test indicator combos in realistic conditions, shorten validation cycles, and preserve profit splits while converting proven setups into real payouts.

Which indicator you favor is less important than how you combine them into rules you can backtest, demo, and size consistently, and how you enforce stops so a few losses do not derail the edge. Keep one core setup mastered for 30 trading days before adding variants, log every trade with the indicator conditions that triggered it, and treat every deviation from the rules as a data point, not an excuse. That feels like a solution, until you run into the one hidden variable that makes or breaks every "leading" signal in live trading.

What is a Day Trading Leading Indicator?

A day trading leading indicator is a short‑term predictive signal you use to anticipate a move before most of the market confirms it, so that you can take a timed entry with defined risk and measurable outcomes. It is not a prophecy; it is a rule: an observable condition you can test, quantify, and hold yourself to under live execution.

How should I test an indicator’s real edge?

When I validate a signal, I treat it like an experiment with fixed variables and pass/fail criteria. According to RayAlgo, 75% of traders use leading indicators for day trading. The first test is statistical, not aesthetic: run a realistic replay or tick-level sim with order types, slippage, and a minimum sample size, then measure expectancy, profit factor, and drawdown. Insist on at least 200 trades across varying volatility days before calling a result trustworthy, and log the exact filter that triggered each trade so you can reproduce winners and failures.

When do leading indicators break down?

This problem appears across stocks, futures, forex, and crypto: signals flip to noise when market structure collapses into chop or when exogenous events flood the tape. In practice, that looks like a flurry of setups that stop out for similar losses, where execution and spread widen, and the indicator’s hit rate collapses. Protect yourself by treating live failure modes as data, not excuses, and by recording how often signal quality drops on news days or in low liquidity windows.

How do you combine indicators into objective rules?

If your checklist reads like a wish list, it will fail under pressure. Over 50% of successful day traders rely on a combination of leading indicators to create redundancy and reduce false breaks, according to over 50% of successful day traders rely on a combination of leading indicators. Build combinations as explicit gates, for example: signal A must trigger, volume must be above a rolling 20‑period average by a defined z‑score, and a fast momentum oscillator must confirm within three bars. Turn every element into a binary pass/fail so your backtest and your live journal speak the same language.

Most teams handle validation with scattered spreadsheets and ad hoc sim runs, because it feels familiar and requires no process change. That approach works early, but as you try to scale a repeatable edge, it fragments evidence, drags validation from days to weeks, and buries why a setup failed in production. Platforms like AquaFutures provide instant simulated capital and structured evaluation rules that compress testing cycles from weeks to days, let you validate indicator combinations under realistic order execution, and preserve trader profit splits while turning a proven checklist into a pathway for funded payouts.

What operational checks keep a leading signal honest?

Treat the indicator as one component of an operational stack: execution plan, slippage budget, size rules, and stop logic. Require defined order types and pre‑set slippage limits in the sim, quantify realized slippage as a percentage of the target, and fold that into position sizing. Add a timing filter, for example, only act on signals in the first 90 minutes of U.S. cash open or during London session overlap for FX, because signal reliability shifts by session. Use cluster logic to reduce noise, for instance, only trade when the same trigger appears twice within a short bar window and the second trigger arrives on higher volume.

How do you measure whether a leading indicator is scalable?

This is a constraint problem. Some signals work well at small sizes and break down when legged up; others hold up to scaling but require wider stops. Test scalability by running a volume‑sweep sim: increase notional in steps and watch capacity, slippage, and execution fill rates. Your objective metrics should include profit factor, expectancy per trade, and a stability score across three liquidity regimes. If expectancy stays positive and drawdown behavior remains consistent as size rises, the signal is likely scalable.

Think of a leading indicator like a carefully tuned smoke detector, not a fire forecast: you want it sensitive enough to warn you early, but calibrated so household cooking does not trigger a panic and ruin the evening. That balance—the sensitivity you need, the noise you can tolerate, and the execution plan you commit to—separates hobby setups from consistent, scalable strategies. That apparent edge holds until you discover the single variable that quietly decides whether signals become repeatable payouts.

Related Reading

- What Is a Funded Trading Account

- What Is SMT in Trading

- Price Action Trading

- Intraday Trading Tips for Today

- Can Day Trading Be Profitable

- Trading Indicators

- Forex Trading Candlestick Patterns

- Intraday Algorithmic Trading

- Trading Candlestick Patterns

- Volatility Trading

Why Do Day Traders Need Leading Indicators?

Leading indicators matter because they let you turn anticipation into an operational rule set you can measure, size, and repeat under live constraints. They are not about mystical timing; they are about keeping entries small, defined, and verifiable so your short-term edge converts into consistent outcomes.

How do leading indicators change execution in real time?

They force you to specify execution primitives up front, such as exact order types, acceptable slippage, and a clear time-to-fill window. Treat each signal as an execution request with a checklist: order type, target spread, max slippage, position size, and a hard time cutoff. That transforms a fuzzy hunch into a reproducible instruction a trader or algo can follow, and it limits the human temptation to widen stops after a losing streak.

What operational metrics tell you the indicator is honest?

Track hit rate, average reward to risk, realized slippage as a percent of target profit, and how expectancy changes when you scale size across three liquidity regimes. Add a decay metric, the rate at which signal performance falls over rolling 30, 60, and 90-day windows, and a false positive frequency so you know how often the indicator produces identical stop losses. Run these as daily control charts, so you see drift before it becomes a drawdown.

Why do you need regime detection and adaptive thresholds?

Signals that worked yesterday often fail when volatility, spread, or session flow shifts. Build a simple regime detector, for example, a volatility z-score and a liquidity filter, then change your thresholds when the detector flips. In practice, that means wider stop budgets on high-volatility days, tighter entry gates in low-volume sessions, and automatic session filters that only allow your setups during proven windows.

Most traders validate setups with spreadsheets and scattered sim runs because it is familiar and low cost, but that approach fragments evidence and stretches verification from days into weeks, creating inconsistent decisions under pressure. That familiar approach works early, but as signal frequency and stakes rise, the hidden cost becomes apparent: fragmented backtests, inconsistent execution rules, and wasted time reconciling why live results differ from simulated results. Platforms like AquaFutures provide instant simulated capital, realistic order execution testing, and structured evaluation rules that compress validation cycles, so traders can prove a rule set under pressure and convert it into funded payouts faster.

How should you guard against the two most painful failure modes?

First, stop treating the indicator as the decision and start treating it as a testable hypothesis with pass/fail gates. Second, log every trade with exact pre-trade conditions, then run post-trade audits weekly to check for contamination, rule drift, or behavioral overrides. Make the audit mechanical: if any trade violated the checklist, mark it, quantify its cost, and exclude it from performance until the setup is adjusted.

History favors systems that survive scaling and time, not one-off wins, which is why prudence in validation matters now more than ever, as [Obside, 2025-09-02, "Long-term trading strategies have historically outperformed short-term strategies by 15% annually. That longer view of repeatability is visible even at the portfolio level, a point underscored by Obside: "Over 70% of long-term investors have seen positive returns over 10 years", which reminds you that converting intraday edges into lasting performance requires discipline, monitoring, and scalable confirmation.

When the signal starts to fail, treat it like equipment showing wear, not a personal failing; diagnose whether the problem is execution, market regime, or checklist erosion, then repair one variable at a time. Think of a leading indicator like a pit crew instrument, calibrated, logged, and judged by how well it helps you leave the pits on time. There is more that breaks quietly than you expect, and the next part uncovers the one limitation that can turn a working system into a trap.

Limitations in Using Leading Indicators and How to Overcome Them

Leading indicators fail most often because they are treated as verdicts rather than experiments, and you fix them by measuring, validating, and enforcing simple operational rules that keep their signal honest. Do the statistical work up front, automate routine checks, and impose human review gates so an indicator becomes a reliable tool you can scale, not a noisy temptation that erodes capital.

How do you know an indicator actually adds measurable value?

Start with a compact KPI set that answers three practical questions: does it predict before the move, how often is it right, and does it improve net expectancy after costs. I track lead time, precision (true positives over all positives), conditional expected net of slippage, and a lift metric relative to a randomized baseline. Use bootstrapped confidence intervals for the expectation to show uncertainty, not a single-point estimate, and set a minimum sample size before declaring a pass. Treat those metrics as go/no-go gates, not soft suggestions.

Why is measurement so fragile in live trading?

This problem occurs across traders and small teams: you can build a clean backtest, but when live conditions change, the metric disappears. That measurement gap mirrors broader organizational struggles, captured by OSHA (2019), "50% of organizations report difficulty in measuring the effectiveness of leading indicators", which explains why many setups look great on paper but fail under real conditions. The culprit is rarely the math alone; it is look-ahead bias, sample selection, and failing to fold in execution costs when you report hit rates.

How do you prevent overfitting and keep an indicator honest?

The failure point is almost always parameter hunting. Use strict out-of-sample walk-forward testing, then validate with a non-overlapping live replay. Penalize complexity with information criteria, and insist on parameter stability across at least three different liquidity regimes before you scale size. If a parameter moves widely when you re-run a short window, retire or fence the setup until you can explain the drift. Think of it like keeping a radio dial tuned, not re-engineering the receiver every time reception wavers.

What operational rules stop signal degradation?

When we ran a 14-day controlled replay with a small group of candidates, the pattern became clear: premature re-tuning after a few losses is the fastest way to destroy a signal. Implement a maintenance cadence, for example, a monthly performance audit and an automatic alert when lead-time or lift drops more than 20 percent versus baseline. Enforce human sign-off for any parameter change and require at least 50 new trades under the new setting before counting those results. Those constraints convert fiddling into disciplined calibration.

Most traders manage tuning with spreadsheets and ad hoc replay because it is familiar and low cost, and that works at first. But as tests multiply and stakes rise, evidence fragments, re-testing slows, and you end up chasing noise instead of improving signal quality. Platforms like funded accounts for futures trading centralize simulated capital, structured evaluation rules, and automated walk-forward testing, so teams can compress iteration time, maintain a single source of truth for performance, and recalibrate only when objective thresholds are triggered.

How should you test capacity and real-world execution limits?

Treat capacity as an operational variable. Run stepped notional tests that simulate increasing participation rates, measure realized slippage and fill probability, and record how expectancy changes as you scale. Model order-book impact by replaying historical depth, if available, and prefer limit-participation algorithms to blunt market impact as you scale. If the expected value falls below your cost-adjusted threshold as size increases, the setup has reached its market capacity and should be limited or split across instruments.

How do you protect traders from the emotional cost of noisy signals?

It is exhausting when setups flood the screen with false positives and lead to overtrading. Reduce alert fatigue with a simple gate: a signal only notifies the trader if two independent conditions pass within a short window, and cap daily alerts per strategy to a small, tradeable number. Require a short cool-off period after three consecutive misses to prevent human behavior from amplifying noise. Log every deviation from the checklist, then use those logs in your monthly audit to diagnose whether failures were model issues or behavioral overrides.

What reporting and governance keep indicators reliable over time?

Run rolling performance heatmaps and a decay metric that reports how expectancy changes over 30, 60, and 90-day windows; if decay accelerates, trigger a root-cause review. Keep versioned parameter histories with timestamped notes explaining why changes were made, and make your go/no-go thresholds public to anyone on the desk so adjustments are transparent. That governance transforms an indicator from a private hunch into an auditable trading instrument that can win funding and scale. This is where maintenance becomes strategy, not an afterthought. But the frustrating part? This isn't even the most complex piece to figure out.

Related Reading

- Basic Trading Strategy

- Spot Algorithmic Trading

- Forex Trading Profit Per Day

- Crypto Trading Bot Strategies

- Best Forex Trading Bots

- Fair Value Gap Trading Strategy

- Best Indicators for Swing Trading

- Best Charting Software for Day Trading

- Best Indicators for Options Trading

Practical Applications of Leading Indicators for Day Trading

Leading indicators become useful in day trading when you turn them into tight, actionable rules that tell you exactly what to do, when, and how much to risk. Treat them as short, measurable experiments: scan, execute with a fixed order type, log outcome, and repeat until the signal proves durable under realistic fills.

Which microstructure and intermarket cues actually move price before the crowd?

Pattern recognition matters here. Watch pre-market trade-book imbalance, cumulative delta shifts, and option-skew flips for early conviction, because these signals show where liquidity is preparing to flow. A practical rule I use: if pre-market depth shows the ask side thinning by a 3:1 ratio versus bid within 30 minutes of the open, plan a laddered entry above the pre-market high with two staggered limit orders and a stop below the low of the imbalance bar, sizing so the first fill risks 0.25 percent of equity. That converts an ambiguous lead into an execution plan you can test in a replay or sim. Think of it like watching a theater audience stand up in a cluster before the applause; you want to be at the exit, not still in your seat.

How should you translate tiny lead times into scaling and stop rules?

Constraint-based thinking helps. If a signal gives you only two to five bars of lead time, favor small, mechanical entries, immediate hard stops, and quick partial scales rather than wider bets. When we ran a seven-day controlled replay with four traders and stepped notional from micro to small size, the pattern became clear: doubling size without widening stop budgets halved fill quality and erased edge. Use stepped participation; increase size only after confirming fill rates remain above a target; and tie stop placement to visible book resistance rather than arbitrary ATR multiples. That way, you test capacity before committing larger capital.

Most traders trust spreadsheets and manual replay because they are familiar, but that habit fragments evidence as complexity grows, costing time and obscuring why a setup fails. The hidden cost is slow, noisy validation that loses you opportunities to prove an edge while market regimes shift. Platforms like AquaFutures centralize simulated capital, realistic execution testing, and pass/fail evaluation gates, compressing iteration time so traders can prove a rule set faster and present reproducible results for funding consideration. This flow aligns with how professional desks evaluate capacity and consistency. This approach is why structured validation matters to short-term profitability, and OpoFinance Blog, "Traders using leading indicators report a 25% increase in profitability." supports the case for disciplined proof over intuition.

What operational checks stop good-looking leads from decaying into losses?

Build two defenses: a real-time regime detector and a contamination audit. The regime detector can be a simple volatility z-score against a 20-period baseline plus a liquidity filter tied to average depth, and it should automatically widen or close your gates when the detector flips. The contamination audit is a weekly pass in which you mark any trade that violated its pre-trade checklist and remove those trades from your performance until revalidation.

This keeps parameter hunting in check and forces you to treat the indicator as equipment, not a verdict. Practical test: require at least 100 checklist-compliant trades in a simulated environment, then run a stepped-size replay to confirm stability under increasing participation, because reproducibility under cost is the real filter between a hobby edge and a bankable one, supported in practice by evidence that structured leading signals lift success rates, as seen in OpoFinance Blog, "Leading indicators can improve trading success rates by up to 30%."

It is exhausting when setups trigger constantly without clear rules, and you end up overtrading. Simplify alerts so a strategy notifies you only when two independent gates pass within a short window, cap daily signals per strategy, and enforce a cool-off after three straight misses. Those guardrails preserve capital and mental bandwidth so a single working setup can be scaled cleanly. Once you prove an indicator under realistic fills, the remaining question is not whether it works, but how you capture that proof in a way that wins funding and sustains growth. What traders discover when money is cheaper than patience will change how you validate every edge.

Related Reading

- Fibonacci Trading Strategy

- Best Prop Trading Firms

- ORB Trading Strategy

- Crypto Swing Trading Strategy

- Best Copy Trading Platform

- Best Proprietary Trading Firms for Beginners

- Best Stocks for Options Trading

- Silver Bullet Trading Strategy

- Order Block Trading Strategy

- The Strat Trading Strategy

- Supply and Demand Trading Strategy

- Profitable Gold Trading Strategy

- Higher High Lower Low Trading Strategy

Unlock up to 50% off Your First Funded Account for Futures Trading

Most traders I work with prove an RSI or MACD setup in sim and then hit a funding bottleneck that keeps a tested edge off the tape. If you want to convert indicator-validated rules into live, scalable capital sooner, consider AquaFutures, which offers fast funded accounts with simple, transparent rules, weekly payouts, and limited-time incentives like up to 50 percent off your first account plus rotating BOGO bonuses.